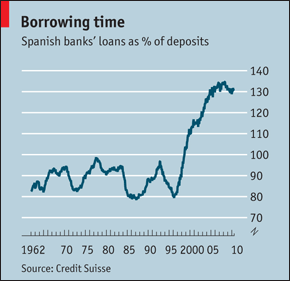

This chart from a September 30, 2010 Economist article (“Two Cheers, Three Tiers”) sums up the significant risk building up in Spain’s banking system.

As suggested in the chart, Spanish banks’ loans as a percent of deposits have leapt to approximately 130% over the last decade. This 30% gap has been filled by wholesale financing, which tends to be much less sticky than retail deposits (think Lehman or Bear Stearns, which faced a massive run when their access to the capital markets dried up essentially over night). While the larger and healthier Spanish banks have been able to access wholesale financing (albeit at higher rates), the vast majority of the country’s financial institutions have been shut out of this market. As such, the country is in the midst of a severe deposit war, with the Economist suggesting that “banks are trying to claw share from the beleaguered cajas by offering rates as high as 4%. Higher funding costs are squeezing net interest margins, which fell by 6.4% in the first half of the year for the banks and by nearly a quarter for cajas.”

As suggested in the chart, Spanish banks’ loans as a percent of deposits have leapt to approximately 130% over the last decade. This 30% gap has been filled by wholesale financing, which tends to be much less sticky than retail deposits (think Lehman or Bear Stearns, which faced a massive run when their access to the capital markets dried up essentially over night). While the larger and healthier Spanish banks have been able to access wholesale financing (albeit at higher rates), the vast majority of the country’s financial institutions have been shut out of this market. As such, the country is in the midst of a severe deposit war, with the Economist suggesting that “banks are trying to claw share from the beleaguered cajas by offering rates as high as 4%. Higher funding costs are squeezing net interest margins, which fell by 6.4% in the first half of the year for the banks and by nearly a quarter for cajas.”

While drawing too many parallels to Ireland may be a bit premature, its important to note that Ireland’s bailout was precipitated by the rapid loss of retail deposits from the nation‘s largest banks. As an example, Allied Irish lost €13 billion ($21 billion) of deposits since the beginning of the year. Investors fearing contagion to Spain should monitor carefully the deposit levels in the country’s banking system.

As if the deposit war isn’t concerning enough, the Economist concludes the article by commenting “that banks still have €323 billion of exposure to property developers, which for some is close to four times their core capital.”

As suggested in the chart, Spanish banks’ loans as a percent of deposits have leapt to approximately 130% over the last decade. This 30% gap has been filled by wholesale financing, which tends to be much less sticky than retail deposits (think Lehman or Bear Stearns, which faced a massive run when their access to the capital markets dried up essentially over night). While the larger and healthier Spanish banks have been able to access wholesale financing (albeit at higher rates), the vast majority of the country’s financial institutions have been shut out of this market. As such, the country is in the midst of a severe deposit war, with the Economist suggesting that “banks are trying to claw share from the beleaguered cajas by offering rates as high as 4%. Higher funding costs are squeezing net interest margins, which fell by 6.4% in the first half of the year for the banks and by nearly a quarter for cajas.”

As suggested in the chart, Spanish banks’ loans as a percent of deposits have leapt to approximately 130% over the last decade. This 30% gap has been filled by wholesale financing, which tends to be much less sticky than retail deposits (think Lehman or Bear Stearns, which faced a massive run when their access to the capital markets dried up essentially over night). While the larger and healthier Spanish banks have been able to access wholesale financing (albeit at higher rates), the vast majority of the country’s financial institutions have been shut out of this market. As such, the country is in the midst of a severe deposit war, with the Economist suggesting that “banks are trying to claw share from the beleaguered cajas by offering rates as high as 4%. Higher funding costs are squeezing net interest margins, which fell by 6.4% in the first half of the year for the banks and by nearly a quarter for cajas.” While drawing too many parallels to Ireland may be a bit premature, its important to note that Ireland’s bailout was precipitated by the rapid loss of retail deposits from the nation‘s largest banks. As an example, Allied Irish lost €13 billion ($21 billion) of deposits since the beginning of the year. Investors fearing contagion to Spain should monitor carefully the deposit levels in the country’s banking system.

As if the deposit war isn’t concerning enough, the Economist concludes the article by commenting “that banks still have €323 billion of exposure to property developers, which for some is close to four times their core capital.”